Want to discover how AI is redefining professional services and client impact?

Join us at the TechEquity Ai Summit 2025 to hear from founders, investors, and industry leaders who are shaping the next wave of AI adoption in consulting, compliance, law, and enterprise services.

Location: Plug and Play Tech Center, Sunnyvale, CA

Location: Plug and Play Tech Center, Sunnyvale, CA Date: November 7–8, 2025

Date: November 7–8, 2025 Register now: techequity-ai.org/registration

Register now: techequity-ai.org/registration

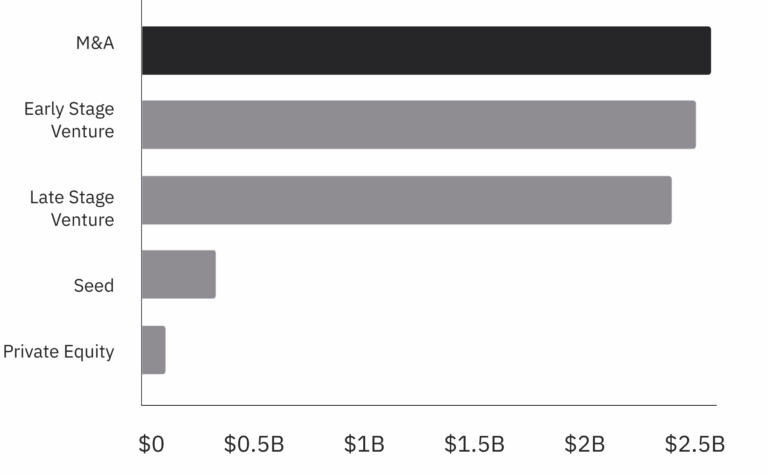

Source note: All funding amounts and company totals cited in this article, unless otherwise attributed, are drawn from Crunchbase data as of 2025.