Pathos, Hippocratic AI, and Plenful headline a fresh wave of AI-in-healthcare deals in 2025—together raising $556M to accelerate drug discovery, clinical decision support, and automated operations across the care continuum.

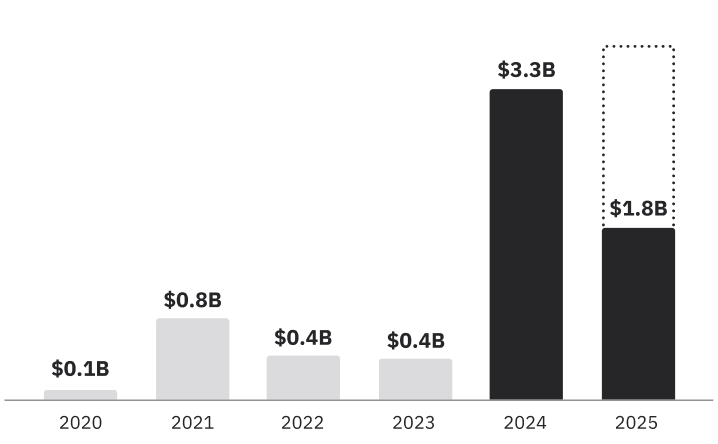

The funding picture: 2020 → 2025

AI in healthcare has entered a new investment era. After years of modest growth, 2024 marked an all-time high with $3.3 billion in venture funding. And 2025 is showing no signs of slowing down—$1.8 billion has already been raised in the first half of the year.

- 2020: $0.1B

- 2021: $0.8B

- 2022: $0.4B

- 2023: $0.4B

- 2024: $3.3B

2025 (YTD): $1.8B (dashed bar indicates potential upside later this year)

So what’s driving this surge? Investors are increasingly looking toward AI not just for incremental efficiencies, but for transformational change across diagnostics, drug discovery, care delivery, and digital health infrastructure.

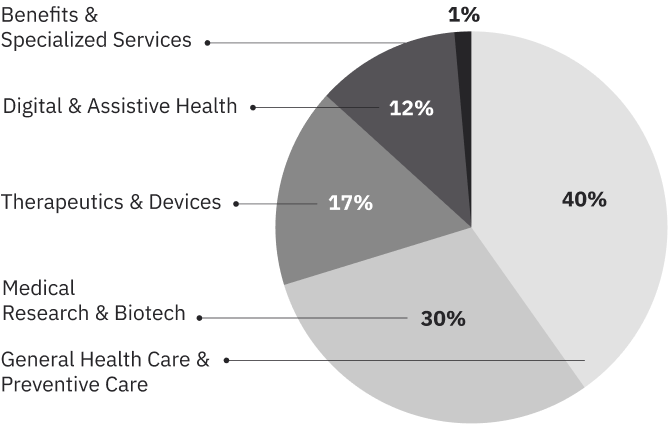

Where is healthcare AI funding going?

The AI healthcare market in 2025 is not a monolith. It’s a complex ecosystem, and venture capital is flowing into a wide range of subcategories:

- General health care and preventive care – 40%

- Medical research and biotech – 30%

- Therapeutics and devices – 17%

- Digital and assistive health – 12%

- Benefits and specialized services – 1%

Infrastructure Over Point Solutions The 40% allocation to general healthcare and preventive care shows investors are backing horizontal platforms that can scale across multiple healthcare segments. This reflects a clear preference for broad-reach solutions over niche applications.

Research Pipeline Maturation With 30% flowing to medical research and biotech, investors are validating AI’s proven ability to accelerate drug discovery. This substantial allocation indicates confidence that AI can meaningfully compress development timelines and improve success rates.

Care Delivery Transformation Combining therapeutics/devices (17%) and digital health (12%) equals 29% – nearly matching research investment. This suggests equal opportunity exists in transforming existing care workflows versus discovering new treatments.

Administrative AI Saturation The minimal 1% allocation to specialized services signals either market saturation in administrative healthcare AI or investor skepticism about sustainable business models in this space.

The heavy concentration in general platforms indicates a consolidating market where scale and network effects will determine winners. Investors are betting that broad healthcare AI platforms will capture disproportionate value, similar to patterns we’ve seen in other AI-driven industries.

This distribution suggests healthcare AI is evolving from experimental point solutions toward platform-based infrastructure plays that can transform entire care ecosystems1.

What’s driving AI adoption in healthcare?

Three clear forces are pushing healthcare AI forward in 2025:

Breakthroughs in drug discover

AI is accelerating research and development, enabling faster identification of promising drug candidates. From compound screening to molecular design, machine learning is shaving years off traditional development timelines.

Diagnostics and clinical tools

Hospitals and care systems are integrating AI into imaging, pathology, and triage. These tools improve accuracy and speed, helping clinicians make better decisions and streamline patient care.

Growth in digital health and wearables

With increased availability of patient-generated health data, AI is playing a growing role in early detection, behavior tracking, and remote care. This shift supports more proactive and personalized health interventions.

Companies leading the 2025 funding surge

While the broader sector is expanding, a handful of startups are emerging as category-defining leaders. These companies have secured significant funding in the first half of 2025 and are building infrastructure for what could be the next generation of healthcare AI.

1. Pathos

In May 2025, Pathos raised $365 million in Series D funding.

Series D | Total funding: $447M

Pathos applies AI across the drug-development stack—from target identification and molecule design to preclinical candidate selection—aiming to trim cost and time to IND. The company emphasizes model interpretability, integrating multi-omics and real-world data to prioritize higher-probability programs. Fresh capital is aimed at expanding wet-lab automation, adding therapeutic area leads, and scaling strategic pharma collaborations to move more assets into the clinic.

In January 2025, Hippocratic AI secured $141 million in Series B funding.

Series B | Total funding: $276M

Hippocratic AI builds domain-safe, healthcare-tuned generative agents for frontline and back-office workflows. The platform focuses on high-stakes reliability—guardrails, red-team evaluation, and role-specific competencies—so nurses, care coordinators, and revenue-cycle teams can offload repetitive tasks without sacrificing quality. The round supports deeper EHR integrations, broader agent coverage (from triage to follow-up), and outcome studies to quantify savings and patient-experience lift.

3. Plenful

In April 2025, Plenful raised $50 million in Series B funding.

Series B | Total funding: $76M

Plenful targets the operational backbone of healthcare—prior auth, referrals, scheduling, and eligibility—with AI-assisted workflow automation. Its approach combines document intelligence, rules engines, and human-in-the-loop review to reduce denials and accelerate reimbursement. New funding is geared toward expanding payer and clearinghouse connections, adding specialty-clinic templates, and launching analytics that surface leakage, bottlenecks, and ROI dashboards for revenue-cycle leaders.

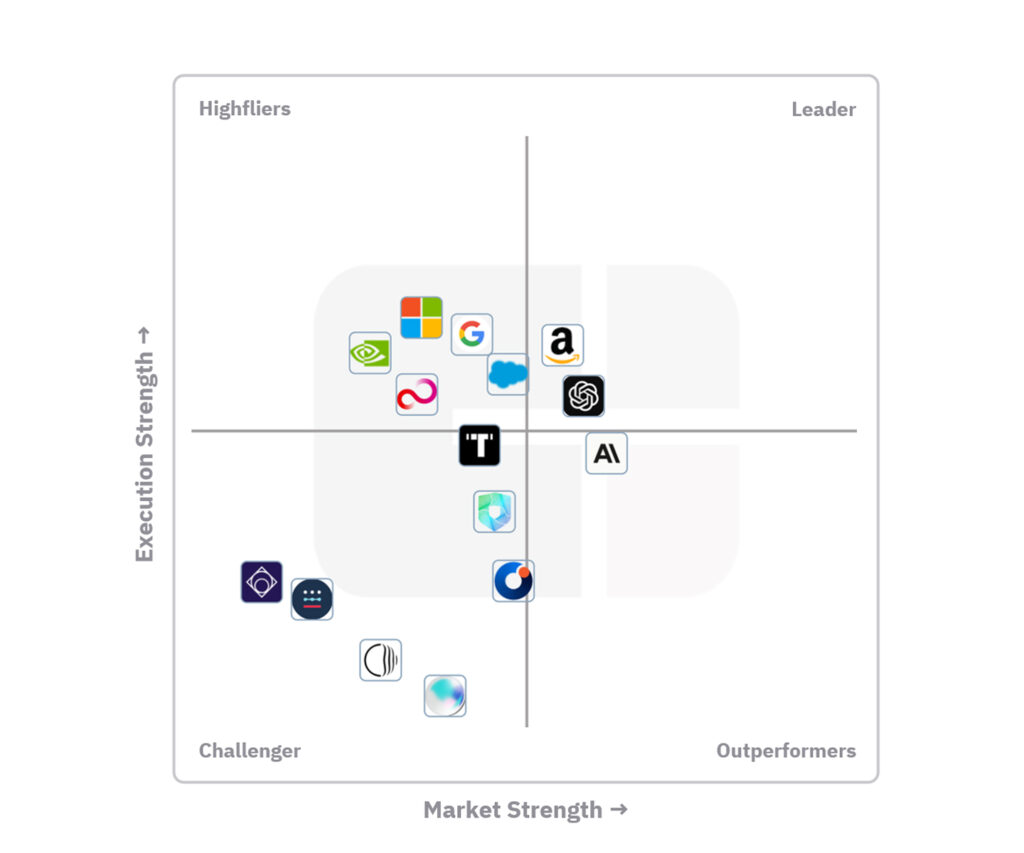

Current major AI players in the healthcare marketplace

The healthcare AI model developers market creates specialized AI models and foundational language models for clinical and administrative healthcare applications2. These companies develop AI systems including large language models, computer vision models, and multimodal AI solutions that address healthcare-specific challenges such as medical imaging analysis, clinical documentation, revenue cycle management, drug discovery, and patient care optimization.

Leader:

- Amazon

- OpenAI

Highflier:

- Salesforce

- Microsoft

- NVIDIA

- Fujitsu

Outperformer:

- Anthropic

Challenger:

- Tempus

- Hippocratic AI

- Aidoc

- Owkin

- Corti

- AKASA

- HOPPR

Join the conversation this November

Want to learn what’s next in healthcare and AI?

Join us at the TechEquity Ai Summit 2025 to hear from founders, researchers, and investors who are shaping the future of biotech, diagnostics, and care.

Location: Plug and Play Tech Center, Sunnyvale, CA

Location: Plug and Play Tech Center, Sunnyvale, CA Date: November 7–8, 2025

Date: November 7–8, 2025 Register now: techequity-ai.org/registration

Register now: techequity-ai.org/registration

Source note: All funding amounts and company totals cited in this article, unless otherwise attributed, are drawn from Crunchbase data as of 2025.

References:

1. CB Insights. The State of Healthcare AI in 5 Charts. CB Insights Research, 2023. Available at: https://www.cbinsights.com/research/healthcare-artificial-intelligence-ai-market/ (accessed September 24, 2025).

2. CB Insights. Best Healthcare AI Model Developers Companies.Available at: https://www.cbinsights.com/esp/healthcare-&-life-sciences/health-data-&-analytics/healthcare-ai-model-developers (accessed September 24, 2025).